In spite of prolonged low commodity prices, 2016 turned out to be an average year for mergers and acquisitions activity (“M&A”) in the Canadian oil patch. While the nature of transactions may change somewhat, with the worst of the price onslaught apparently behind us, 2017 could end up being a fairly robust year for M&A activity.

This article focuses on oil and natural gas M&A activity involving the purchase of an oil and natural gas producing property or company or the merger of two companies which, as their primary business, produce oil and natural gas.

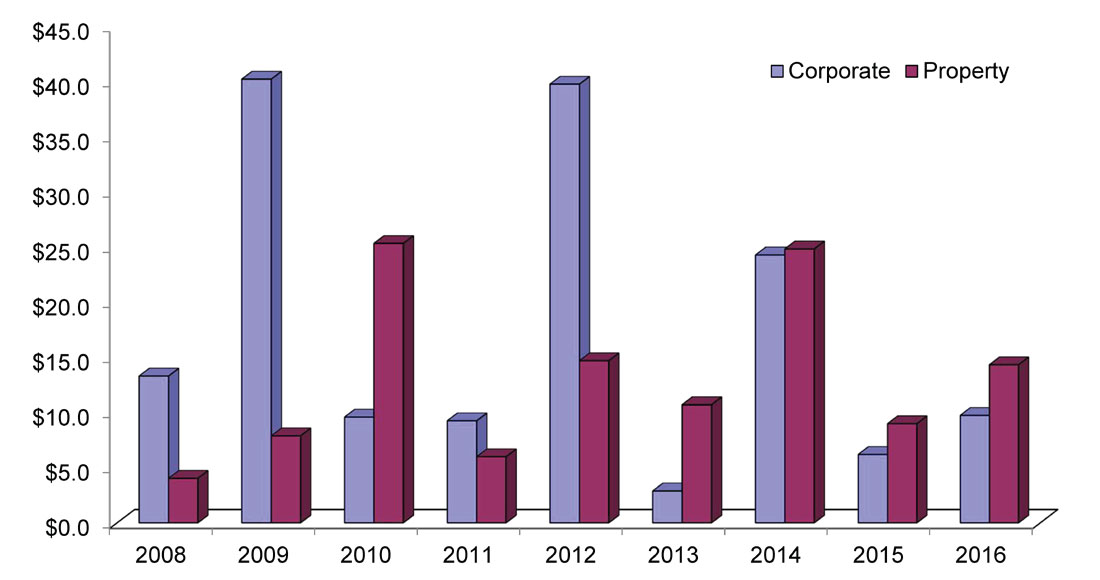

The total value of M&A activity in 2016 was $24 billion, up significantly from the $15 billion in total value in 2015 but down significantly from the $49 billion in 2014. Last year, which was by most measures an “average” year for M&A, saw oil and natural gas assets worth approximately $14 billion and oil and natural gas corporations worth approximately $10 billion change hands.

Sayer’s short term forecast shows continued frothiness in the oil industry, which will impact M&A activity, but the long term forecast shows ample reasons for increased M&A activity. The frothiness is caused by, among other factors, stressed balance sheets of oil and natural gas producers, recent political changes both in Canada and in the United States, an ever increasing focus on environmental issues, and the ongoing pipeline debate.

In 2016 an unprecedented number of oil and natural gas companies became insolvent, with at least 28 companies entering into receivership, bankruptcy or formal financial restructuring processes. Some of the most notable of these companies included Twin Butte Energy Ltd. and Lightstream Resources Ltd.

Twin Butte went into receivership after its stakeholders did not agree to the terms of a proposed restructuring transaction. Twin Butte’s assets are now in the process of being sold to Henenghaixin Operating Corp. through a receivership process.

Lightstream disappeared from the landscape after Ridgeback Resources Inc., a private company owned by former holders of Lightstream’s second lien secured notes, acquired substantially all of the assets of the company through a CCAA process.

There should be a significant decrease in the number of insolvencies in 2017, likely trending downward to the historical average of approximately eight per year. The decrease will be in large part due to the fact that most of the companies which were on the verge of going under either did so in 2016 or found a solution to the problem.

The issue of dealing with suspended wells and other such liabilities, encompassed under the Alberta Energy Regulator’s Licensee Liability Rating (“LLR”) umbrella, will continue to impact M&A activity in 2017. Most severely impacted by these environmental issues will be junior producers, especially those with stressed balance sheets. More mergers of junior entities should result in 2017, in part as a result of the need to get larger in order to be able to financially handle these growing regulatory and environmental issues.

Environmental issues will impact larger entities in different ways, depending upon the nature of the individual company’s assets. Oilsands producers and pipeline companies seem to have the target on their backs right now and for the foreseeable future, with numerous organizations, groups and individuals taking aim.

While on the one hand it appears that our federal government might loosen up the restrictions on the sale of oilsands reserves to international entities, this conflicts with recent comments from the Prime Minister about the future of the oilsands. In December, Natural Resources Minister Jim Carr said that the government is “looking at a far more aggressive trade and investment strategy across the government” and to that end it is reviewing restrictions targeting Chinese investment in the oilsands.

Conflicting Minister Carr’s words of encouragement for investment in the oilsands, in response to a recent question regarding how the government would protect the environment and be aware of climate change while still approving pipelines, our Prime Minister recently remarked that Canada must “phase out” the oilsands.

Increasing pressure from environmental lobbyists and government uncertainty will decrease the appetite for oilsands investments.

The M&A marketplace has recently seen an increase in transactions involving royalty interests, both the acquisition of outstanding royalty interests and the manufacture and sale of a royalty interest on an existing property. This trend, which picked up steam late in 2016, when Pengrowth Energy Corporation, BlackPearl Resources Inc., and Athabasca Oil Corporation announced manufactured royalty transactions on their long-life thermal assets, should continue in 2017. This increase comes in response to a tightening of capital in the equity markets and an increased appetite for oil and natural gas interests that do not have associated environmental liabilities.

Large asset packages should hit the M&A market in 2017 as major international companies review their portfolios and decide to focus on jurisdictions which are financially and politically more attractive than Canada. An example of this is ConocoPhillips, which in November 2016 announced “the initiation of a $5 to $8 billion divestiture program, which will focus primarily on North American natural gas.”

The M&A marketplace should also see more larger attractive asset packages in 2017 than it saw in 2016, as companies with high debt levels will finally shed higher quality assets to fix balance sheets. High quality assets will fetch premium prices in the M&A market, and increased prices should spur other parties to place assets into the marketplace.

Companies with strong balance sheets and good capital market support will use shares as currency in 2017, either to acquire other companies or to acquire assets. There have been a small number of shares for assets transactions recently, with the most notable one being in October 2016 when Tourmaline Oil Corp. acquired assets from Shell Canada Energy for $1.4 billion, paying with a combination of cash and Tourmaline shares.

In the first shares for assets transaction so far in 2017, Craft Oil Ltd. announced earlier this week that it has entered into definitive agreements to sell assets to Cardinal Energy Ltd. and Point Loma Resources Ltd. for a total of $42.6 million (a $41 million sale to Cardinal and a $1.6 million sale to Point Loma), with approximately 90% of the consideration coming in shares of Cardinal and Point Loma.

Capital markets, while continuing to be selective by primarily supporting larger, stronger public entities, should loosen up a bit from the tight levels of 2016. Increased capital availability generally translates into increased M&A activity and increased prices.

All of the aforementioned factors should ultimately result in a robust M&A marketplace in 2017. There will be the traditional slow start to the year, and prices will initially stay low, but as higher quality assets with credible upside hit the market, the buyers will step up to the plate to move average prices back up.

Join the Conversation

Interested in starting, or contributing to a conversation about an article or issue of the RECORDER? Join our CSEG LinkedIn Group.

Share This Article