Introduction

Natural gas is widely regarded as the “clean” energy choice that will power North America until alternative energy sources become widely available. Public reports show Canada’s Federal Government assuming a virtually unlimited supply for the next 25 years 1,2. The US Energy Department assumes Canada’s natural gas exports to the US will grow by 47% in the same time period3. What are the realities of the supply of Canada’s natural gas and what can we as explorationists do to ensure that a shortage of natural gas does not create a North American energy crisis?

My assessments indicate that Canada’s daily average natural gas production peaked in 2001 at 17.4Bcf (493e6m3) per day of marketable gas and that the likelihood of this level being achieved again on a sustainable basis would require an extraordinary effort that is unparalleled in the history of this industry in Canada.

This is an abridged version of an independent study of Canada’s natural gas supply and demand that is now available for industry review.

Current Production Trends

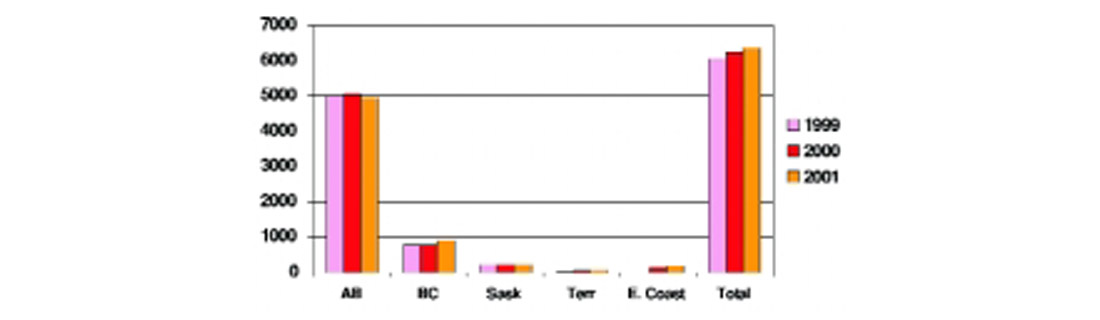

Figure 1 shows actual, marketed gas in Canada for the period 1999 to 2001 derived from CAPP data4. The total marketed gas has increased each year as a result of Ladyfern in BC, the increase in gas production from the Liard and the start of production from Sable Island. However, it should be noted that, each of these activities represent a small fraction of Canada’s total annual marketed gas production of 6.35Tcf (180e9m3) and that few equivalent projects are expected to come on stream in the next few years.

Alberta currently produces nearly 80% of all the natural gas produced in Canada4. This gas is produced from wells that are declining at rates varying from 10% to 50% per year. Over 3Bcf (85e6m3) of new daily gas production must be brought on stream each year just to replace the decline.

The Alberta Energy Utilities Board, using an optimistic assessment of drilling activity, predicts that Alberta’s production will peak in 2004 and slowly decline from that point5. The dominance of Alberta’s production means that any significant decline in Alberta’s production is virtually impossible to make up from other sources.

My assessment suggests that Alberta gas production has already peaked which will likely define the production peak for both Western Canada and Canada as a whole at about 17.4Bcf/d in 2001 (6.35Tcf per year of marketed gas).

(As this paper was going to press (December 2002), the NEB published a new report on natural gas supply14. Their study focused on gas production in Western Canada where they now believe that production peaked in 2001 at 16.6Bcf /day with an expected decline to 15.9Bcf/day by 2004. Restricting the production decline to this level will still require a substantial increase in gas drilling).

New Resources and Reserves

It is important to differentiate between natural gas “resources” and “reserves”:

Resources: The total quantities of natural gas that are estimated, at a particular time, to be contained in known accumulations, plus those estimated quantities yet to be discovered6. Note that there is no implication that these resources are either accessible or producible.

Reserves: Estimated quantities of natural gas recoverable under current technology and anticipated economic conditions from known accumulations. Reliable comparisons must differentiate between initial reserves, remaining reserves and marketable reserves.

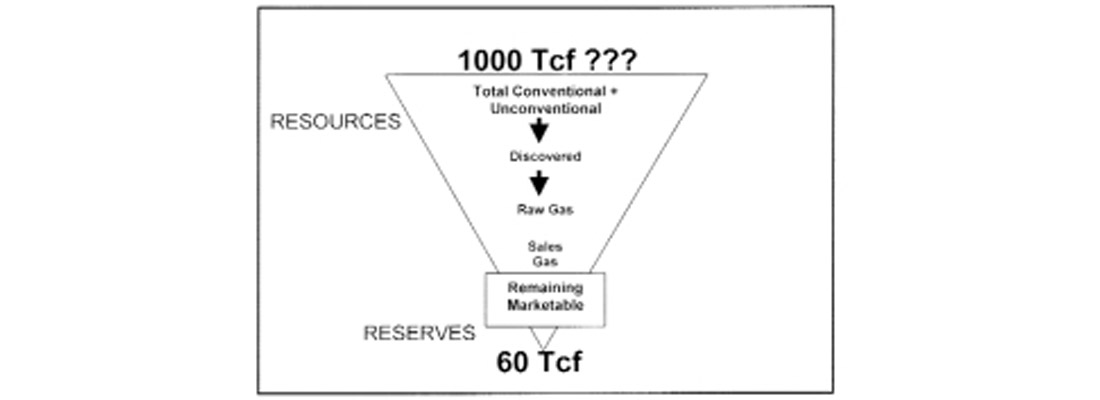

Canada’s total natural gas resources in conventional and unconventional accumulations total in excess of 1000Tcf (28e12m3) (Figure 2). However, the remaining marketable gas reserves – the gas that we can count on producing economically in a reasonable timeframe – currently totals approximately 60Tcf (1.7e12m3); less than ten years supply at current production rates. In reality, as reserves decline, the production rate must also decline so that we can expect lower rate production to continue over many more than ten years.

The Canadian Gas Potential Committee (CGPC) assessed Canada’s gas resources as of the end of 19986. They estimated 592Tcf of conventional gas resources occur in Canada and 246Tcf (7e12m3) of this gas was yet to be discovered. 59% of this undiscovered, conventional gas would come from the Western Canada Sedimentary Basin (WCSB), with the balance from Frontier areas. It must be emphasized that this is strictly an estimate and that there is no guarantee that this gas is either accessible or will be economical to produce. Short-term, the WCSB (primarily Alberta) will continue to be the major contributor to Canada’s gas production.

The Frontier areas of Canada are some of the most difficult areas on earth for exploration and production. Many of these areas are under-explored. Depending on the size of discovery and confidence in future price, they may take many decades to bring on production. These are the orphaned7 or remote6 resources that will have no impact on supply until they have viable access to market. If this gas exists in significant quantity it will be vital that we, as explorationists, find it in the most efficient, cost effective and profitable way.

Coalbed methane and gas hydrates have been touted as unconventional natural gas resources with the potential to supply Canada’s gas needs for many decades. It is undeniable that these resources exist however the technology to economically extract this gas is not yet available. Certainly, as gas prices increase and conventional production declines, we can expect to see greater emphasis on these more technically challenging resources however they are unlikely to provide more than a small percentage of Canadian gas supply during the next decade.

The Bigger Gas Picture

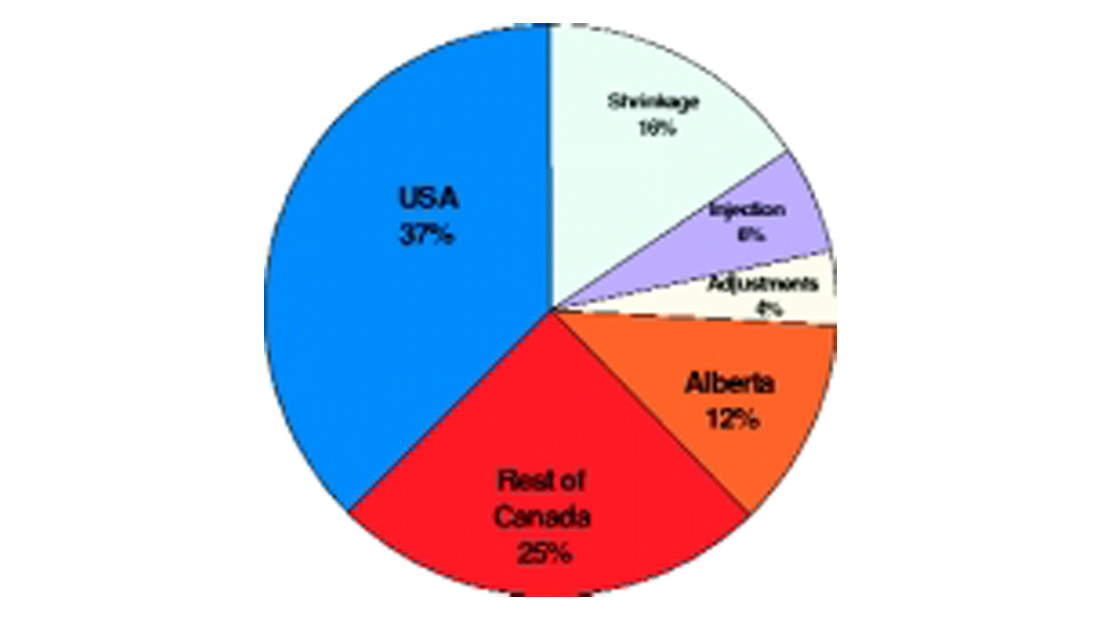

Canada would have ample gas production to supply its domestic needs for many decades; however as Figure 3 shows approximately three-quarters of Alberta’s gas production is actually marketed and half of this is exported to the United States8 where demand for imported gas is expected to continue to increase3. Canadians, particularly Albertans, gain enormous financial benefit from this export. But, how long can this level of export be maintained? Canada is currently the world’s third largest gas producer and second largest exporter; producing about 7% of world production from 1% of the world natural gas reserves9.

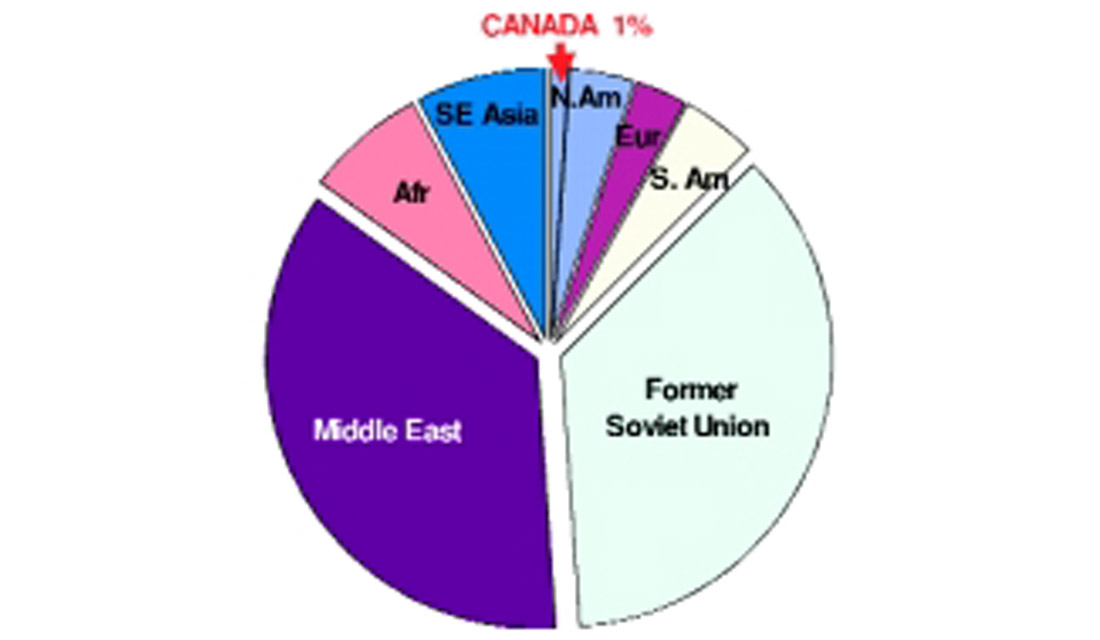

The United States produces about 50Bcf/day (1.4e9m3) and meets its additional demand from Canada and from limited imports of Liquefied Natural Gas (LNG). U.S. Production is expected to decline to 47Bcf/d in 20033; it is not clear how this shortfall will be met. Near-term gas supply shortages are primarily a North American problem where we consume 33% of all the world’s natural gas production yet have about 5% of remaining gas reserves (Figure 4).

The Middle East and Former Soviet Union control more than 70% of the remaining gas reserves9, which suggests as price increases and LNG transport becomes more viable; an ever-increasing portion of North America’s gas needs will be imported from countries that are not particularly sympathetic to our continent. Natural gas will join oil as a world commodity with large volumes traded across continents.

Why is nobody exploring?

Raw statistics would suggest we are excellent at exploration – achieving a 75% success rate in Alberta in 200110. However, closer examination shows that much of this exploration activity is of the “vulture” type11 – close-in exploration that adds short-term deliverability but very little future growth.

Even if we believed all this activity is legitimate exploration, it is startling to find how few major companies are actively exploring in the Western Canada Sedimentary Basin (WCSB). If we consider the growth of income trusts, the disappearance of the mid-sized companies, the focus on short-term results and the increasing interest in international opportunities, there are very few companies with significant domestic exploration departments. If we don’t explore, we cannot add new reserves to sustain future production.

The WCSB has been efficiently explored using modern technology, superior databases and many highly skilled geoscientists. As a result, it has quickly become a mature basin with a deteriorating size of new discoveries.

Many companies believe that the future gas potential of Western Canada is limited and are redirecting their manpower and financial resources to other opportunities – actions that will guarantee a decline in production. If we believe this, we have a responsibility to alert planners and decision makers so that current assumptions on future production can be adjusted.

Alternatively, we can accept the challenge by generating more and better exploration opportunities. There are many ways we can improve our exploration effectiveness12 but they will require a rethinking of our methods individually, corporately and as an industry. Reduced interest in exploration provides an opportunity for skilled explorers and patient investors to achieve excellent results in Western Canada.

Predicting Canada’s Future Natural Gas Production

As some pundit once explained “Predictions are fraught with danger especially when they pertain to the future”. Perhaps, the mere fact that I am publishing this information will cause those with the power to make a difference to act and prove me wrong!

Demand, peace, El Nino, recession, NAFTA, Kyoto, regulatory and environmental issues as well as the whims of politicians and terrorists will all impact our future in ways that are difficult to predict. However, I believe we can make a reasonable forecast of Canada’s future gas supply.

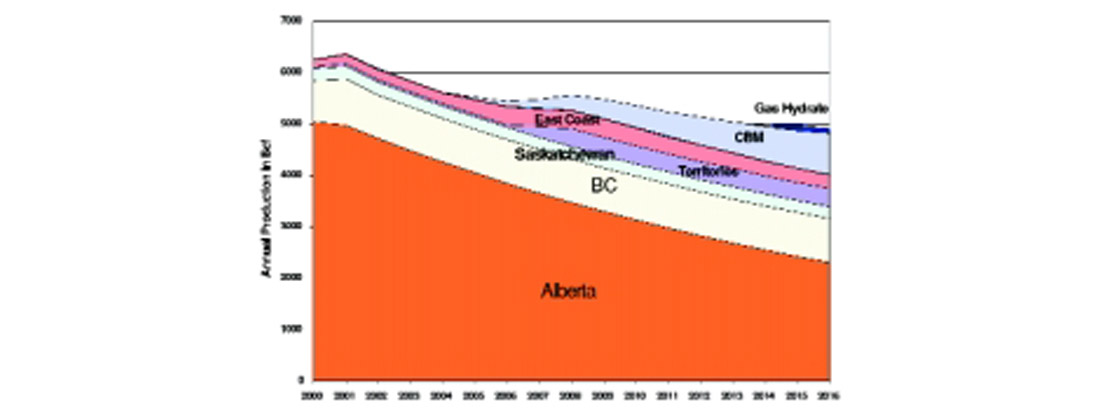

Supply will be dominated by Alberta for the foreseeable future; a 5% annual decline in Alberta’s gas production will occur unless there is a significant increase in quantity and quality of exploration. BC and Saskatchewan may show growth but they will have little impact on the bigger picture. The only substantial conventional gas projects on the drawing board are Deep Panuke (off-shore Nova Scotia) and the MacKenzie Valley pipeline. Add 1.5Bcf/d13 for Coalbed methane and we still get a significant decline in total production (Figure 5). Notice also that the new gas that is replacing our production will be considerably more expensive to develop and produce.

The Alberta Government is meanwhile forecasting a 50% increase in Alberta natural gas demand by 2012 driven by oil extraction at the tar sands, cogeneration and other industrial activities. If this scenario came to pass there would be little gas left for export from Alberta in ten years time. Clearly the story will not play out this way!

Solutions – What can we do?

- This is only a brief overview; a comprehensive study of the current trends and implications is now available. Instant updates can be obtained – visit www.geohelp.ab.ca for more information.

- Average exploration results have been unacceptable. There is much we can learn from this activity. I have developed a number of methods and resources to assist individuals and Companies to achieve better results.

- Geologists and geophysicists have to lead any attempt to add to Canada’s conventional natural gas reserves. We need to be willing to use new and innovative approaches. Are we up to the challenge?

- Either we believe that we can find new reserves of economic gas in Canada or we need to educate the public and politicians to expect a significant decline in supply.

- Regardless of Kyoto, the need for all of us to become more aware of our consumption of this finite resource is imperative.

- Your input and feedback is welcome! Send email to dave@geohelp.ab.ca

Join the Conversation

Interested in starting, or contributing to a conversation about an article or issue of the RECORDER? Join our CSEG LinkedIn Group.

Share This Article