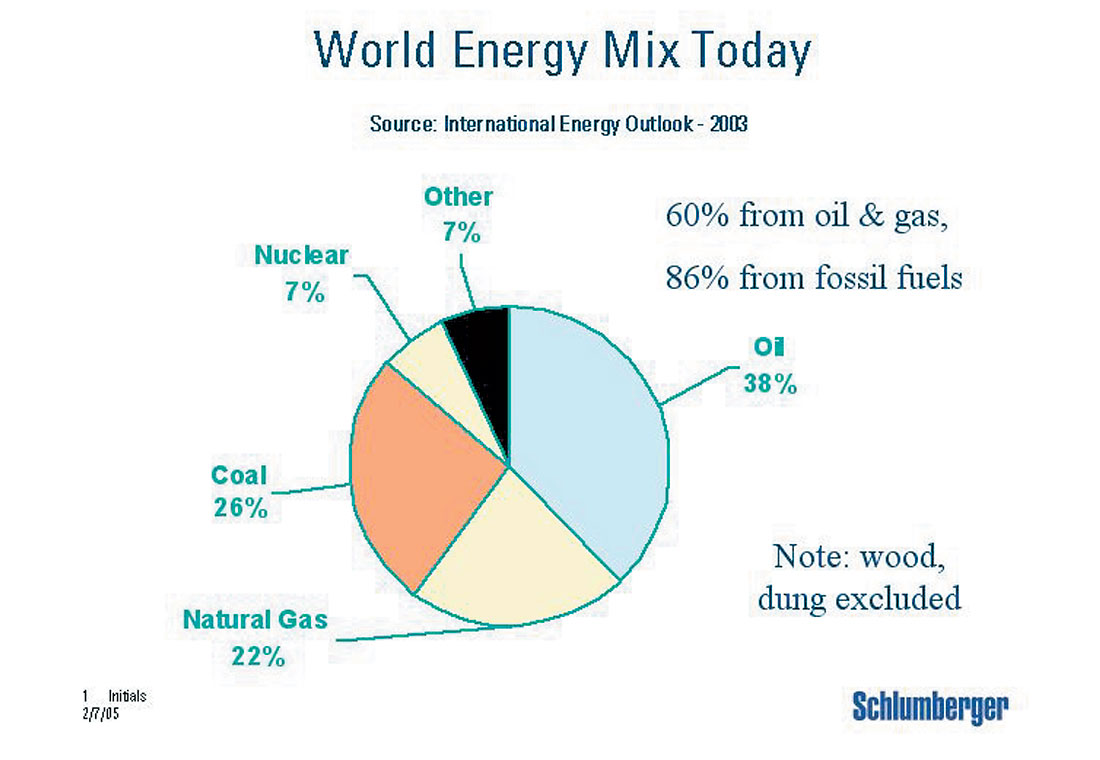

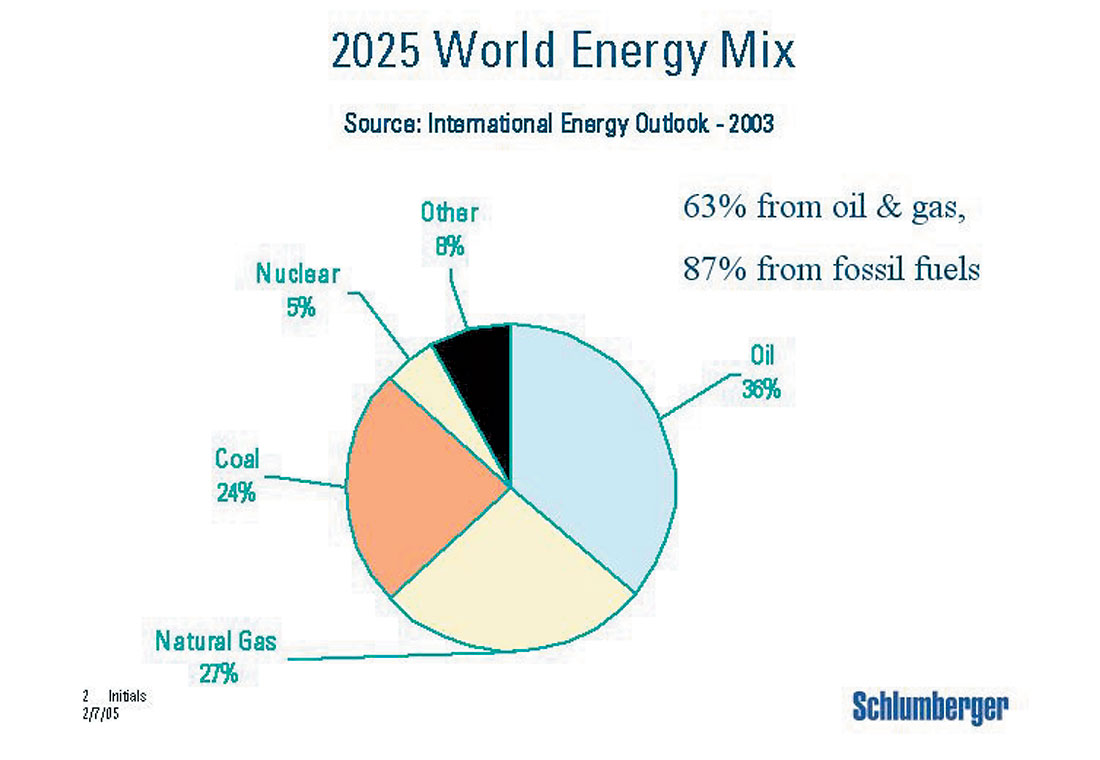

The profession of Geophysics faces significant challenges today. No doubt, the ability of our technology to remotely image the subsurface has provided significant value to the oil and gas industry. The competitive business climate of the oil industry continues to pit geophysical technologies against other alternative means of increasing production and lowering risk and costs. Geophysicists continue to respond with better solutions to E&P needs by providing better, higher- resolution data, more accurate processing and sophisticated integration of seismic data with other reservoir information. Yet, we face significant challenges in the coming years. Today as shown in Figure 1, we get about 86% of our energy from fossil fuels. If we combine the energy needs of developing countries with their growing populations, world energy needs in the next 20 to 25 years are likely to grow by more than 50%. Figure 2 shows estimates from the US International Energy Agency that indicate an even heavier use of hydrocarbons in this period, and in particular, more from oil and gas, even though the growth of alternatives will be significant.

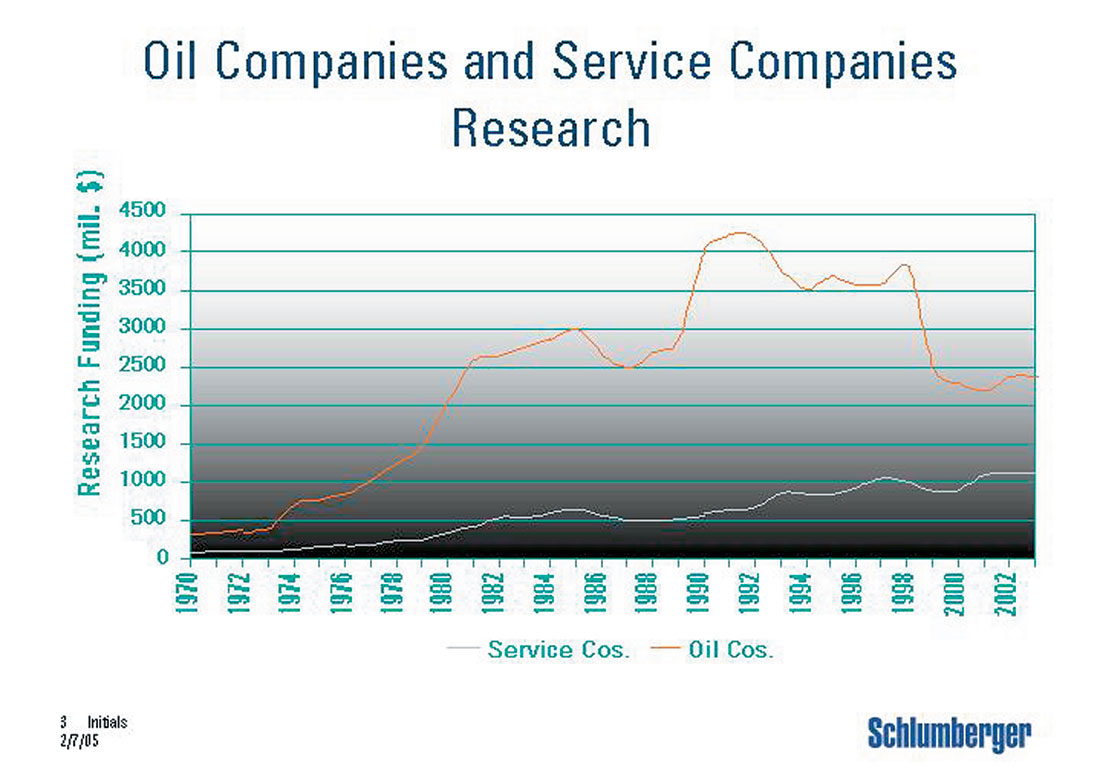

Despite a relatively high and stable oil price, investment to achieve this goal has been restrained. The seismic business remains financially stressed even though seismic information is recognized as the most valuable technology for increasing production and reserves. Service companies have responded by merging and downsizing, creating a challenging job market for geophysicists. At the same time, Figure 3 shows an alarming trend in investment in research and development by oil companies. Note that while such investment has increased in the service sector, these increases do not make up for the decline in spending by oil companies.

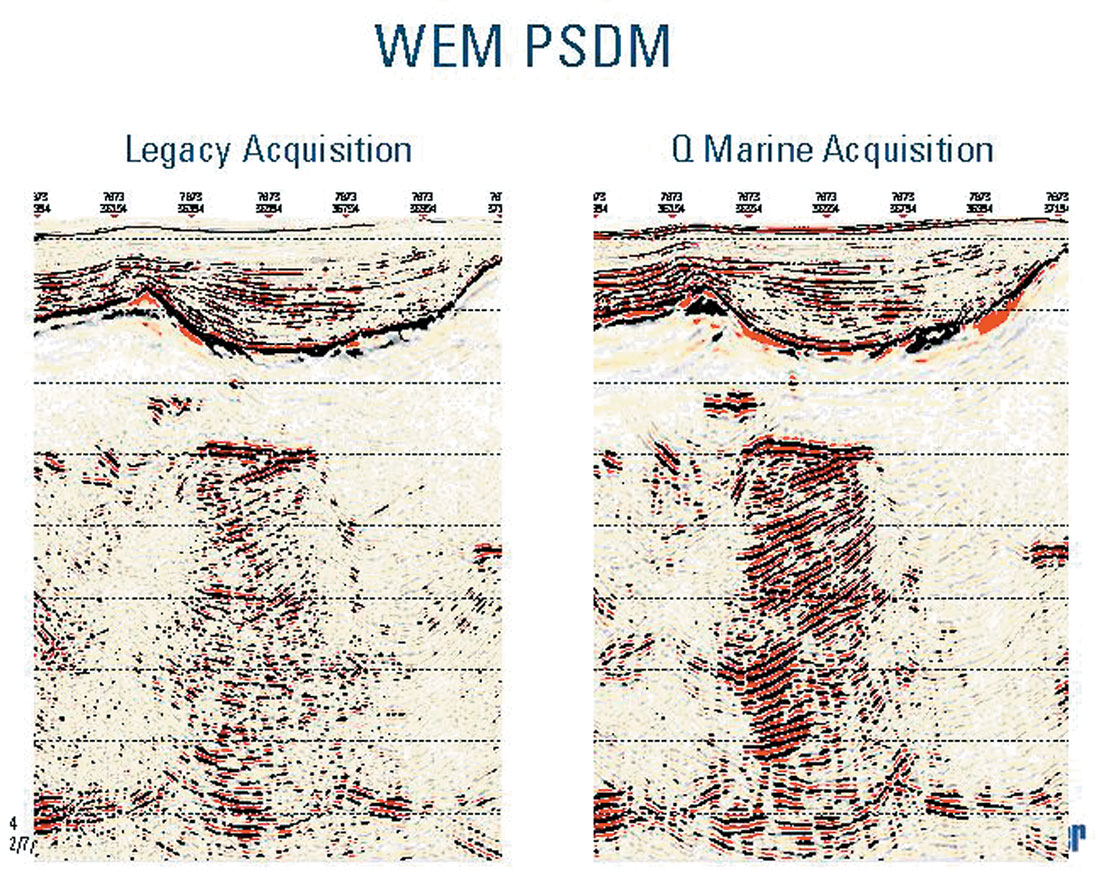

Nevertheless, continued investment by the service companies is yielding better technology. Consider Figure 4 which compares new acquisition targeted at subsalt reflectors with that from just a few years ago. Such clear images of the base of salt and subsalt reflectors are invaluable in mapping and drilling subsalt plays. In general, as we search to develop more difficult prospects and provide more reservoir information, we will likely see a resurgence of acquisition technology wherein acquisition plans and systems are designed to acquire the data needed to solve these specific problems.

Economic forces are thus converging to increase demand for seismic technology in general and more specifically, the demand for leading edge technology and customized solutions will be strong. But to answer the growing energy demands of the world, significant investment will be required in the very near future.

Join the Conversation

Interested in starting, or contributing to a conversation about an article or issue of the RECORDER? Join our CSEG LinkedIn Group.

Share This Article